A financial scam usually becomes obvious too late. The website stops loading. The adviser stops answering. The broker blocks withdrawals. The “tax payment” turns into another fee. The investment account shows a healthy balance, but no money arrives in the bank. At that point, the victim is no longer thinking about returns. They are trying to work out who can help, who to report to, and whether any money can be recovered.

In the UK, the Financial Conduct Authority, or FCA, is one of the main organisations involved when a scam touches financial services. It regulates financial firms and markets, maintains public registers, warns about unauthorised businesses, gathers intelligence, and helps consumers understand what to do after a suspicious approach. The FCA is not the only body involved, but it is usually one of the first places investors should check.

For investors researching markets, brokers and investment products through sites such as Investing.co.uk, FCA checks should be part of the basic process. Reading market news or comparing providers is useful, but it does not replace checking whether a firm is authorised, whether its contact details match the official register, and whether it has been flagged by the regulator.

The blunt version is this: the FCA can help scam victims, but it cannot act as a personal refund service. It can warn, guide, investigate, regulate and share information. Getting money back may depend on the bank, payment method, firm status, police reports, FSCS eligibility, the Financial Ombudsman Service, and how quickly the victim acts. That is not as neat as people would like, but scams are not known for tidy admin.

What The FCA Does For Scam Victims

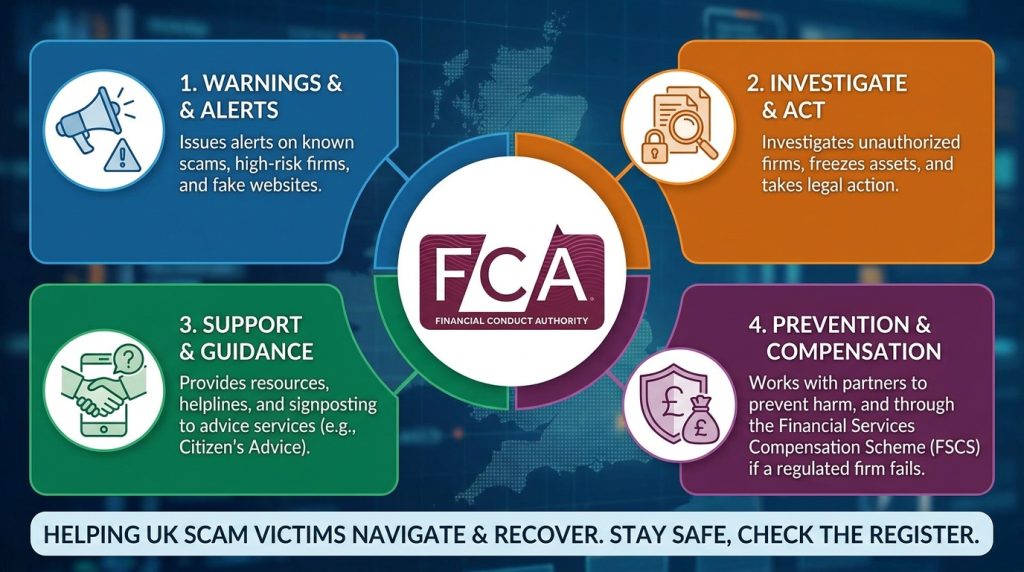

The FCA’s main role is to regulate financial services firms and financial markets in the UK. Its own description says it sets standards for firms and holds them to account, with the aim of supporting a healthy financial system where consumers get a fair deal through the FCA’s role as the UK financial regulator. For scam victims, that role matters in several practical ways.

The first is firm checking. The FCA gives consumers tools to check whether a firm is authorised and whether it has permission to offer the service being promoted. The FCA Firm Checker is designed for exactly this. It helps people check whether a financial services firm is authorised by the FCA and has permission to sell products and services.

This is not just useful before a scam. It is also useful after one. A victim needs to know whether they dealt with an authorised firm, a clone of an authorised firm, or a completely unauthorised business. That distinction affects the next steps. It can influence whether the complaint route is through the firm, whether the Financial Ombudsman Service might be relevant, whether FSCS protection could apply, or whether the matter is mainly a criminal fraud report.

The second role is warning the public. The FCA Warning List lists unauthorised firms and individuals the FCA is aware of. It is not a perfect map of every scam in the country, because new scams appear constantly, but it is still an important tool. If the firm, website, email address or phone number appears on the list, that should be treated as a serious danger sign.

The third role is scam reporting. The FCA’s report a scam guidance explains how consumers can report scams and unauthorised firms to the regulator. The FCA can use these reports to issue warnings, support investigations, identify patterns and work with other agencies. A single report may not bring a victim’s money back, but repeated reports can help expose a wider network.

The fourth role is consumer education. The FCA’s protect yourself from scams guidance explains how to check firms and warns consumers to make sure the firm reference number and contact details match the official FCA record. That detail is critical because many scams do not invent a firm from scratch. They copy a real one.

The fifth role is supervision and enforcement. If an authorised firm is involved in misconduct, the FCA can investigate and take action under its regulatory powers. That does not mean every individual victim receives money directly from an FCA case, but regulatory action can stop harm, lead to public warnings, require firms to change behaviour, and sometimes support redress work.

The FCA therefore helps scam victims by providing structure. It helps answer the first big question: “Who was I really dealing with?” Once that answer becomes clearer, the recovery route becomes less of a fog.

What The FCA Cannot Do

The FCA’s powers are important, but victims need to understand their limits. Expecting the FCA to recover money from every scam is a fast route to frustration.

The FCA does not usually retrieve money from criminals on behalf of individual victims. If money has gone to an overseas fake broker, crypto wallet, personal bank account or unauthorised investment scheme, recovery may depend on banks, payment providers, law enforcement, civil action, asset tracing or whether funds can be frozen quickly. The FCA can receive reports and issue warnings, but it is not a private debt collector with a regulator badge.

The FCA also cannot compensate victims simply because they lost money to a scam. Compensation depends on the facts. Was the firm authorised? Was regulated advice involved? Did a bank fail to handle a scam payment properly? Did a financial services firm fail and leave eligible claims? Each of those questions points to a different route.

The FCA cannot make an unauthorised firm legitimate after the event. If a victim dealt with a fake investment platform that was never authorised, protections such as the Financial Ombudsman Service or the Financial Services Compensation Scheme may not apply to that firm. This is why checking before payment is more useful than checking after the account has vanished.

The FCA also cannot police every online advert, social media account, messaging app group, fake trading platform and cloned website in real time. It can act on intelligence and publish warnings, but scammers move quickly. They change names, domains, phone numbers and payment accounts. The Warning List is helpful, but absence from it does not prove a firm is safe.

This is the part people hate hearing. The FCA is a regulator, not a magic button. It can be very useful, but it cannot undo every payment or force every fraudster to reappear. Victims should use the FCA route, but they should also contact banks, report fraud to police channels, save evidence and escalate complaints where regulated firms are involved.

First Actions After A Scam

The first action is to stop sending money. Scammers often keep victims paying after the first loss. They claim a withdrawal is ready but requires tax clearance, wallet activation, account upgrading, anti money laundering approval, insurance, compliance release, or a final settlement fee. These phrases sound official enough to make a tired victim pause. That is the point. In most cases, another payment is not the path out. It is the next loss.

The second action is to contact the bank, card provider, payment app, crypto exchange or payment service used. Speed matters. If the payment is recent, there may be a chance to stop, recall, freeze, dispute or flag it. Even where recovery is not possible, early notification creates a record and may help stop further payments. With card payments, bank transfers and payment apps, the provider’s fraud team should be contacted directly through official channels, not through numbers supplied by the scammer.

The third action is to secure accounts. Victims should change passwords, enable multi factor authentication, check bank and email logins, remove unknown devices, revoke suspicious crypto wallet permissions, and uninstall any remote access software used during the scam. If identity documents were shared, the victim may also need to monitor credit files and watch for impersonation attempts.

The fourth action is to save evidence. Screenshots matter. Emails matter. Chat logs matter. Payment references matter. Victims should save website addresses, account dashboards, transaction receipts, wallet addresses, phone numbers, names, company numbers, supposed FCA reference numbers, bank account details, contracts, adverts and messages. Fraud websites disappear quickly. Chat groups get deleted. A well organised evidence file makes the next stage less painful.

The fifth action is to check the firm using FCA tools. The FCA Firm Checker can help determine whether the firm was authorised and whether the details match. The FCA Warning List can show whether the regulator has already flagged the firm or contact details. These checks should be saved as screenshots too, especially if they show mismatches.

The sixth action is to report. A financial services scam should be reported to the FCA through the FCA scam reporting page. Fraud and cyber crime should also be reported through Report Fraud in England, Wales and Northern Ireland, while Scotland directs reporting through Police Scotland, usually by calling 101. The GOV.UK online scam and phishing guidance also points victims of online scams or fraud to reporting routes.

The seventh action is to avoid recovery scams. Once someone has been scammed, they may be targeted again. A new person may claim to be from a regulator, lawyer, recovery agency, blockchain tracing company, bank unit or police linked office. They may say the money has been found but a fee is needed to release it. That is often scam number two arriving before scam number one has finished its paperwork.

Checking Firms, Clone Firms And Warning Lists

A large share of investment scams rely on fake credibility. The scammer does not need to build trust from nothing. They can steal it from a real firm.

A clone firm uses the identity of an authorised firm. It may copy the name, logo, address, firm reference number, website design, staff names and legal wording of a legitimate company. The victim checks the name on the FCA register and finds a real result. That creates false comfort. The missing step is checking whether the contact details match exactly.

This is why the FCA tells consumers to check not just the firm name, but also the firm reference number and contact details through its protect yourself from scams guidance. A real firm’s official phone number, email address and website should match the FCA record. If the person contacting you uses a different domain, mobile number, WhatsApp account or payment account, do not wave that away as a harmless branch office.

The Financial Services Register gives public information on firms, individuals and other bodies that are, or have been, regulated by the FCA or the Prudential Regulation Authority. It is the proper place to check authorisation. A certificate attached to an email is not enough. A badge on a website is not enough. A screenshot of a license is not enough. Those things can be copied by anyone with a laptop and the moral range of a damp sock.

The FCA Warning List adds another layer. It identifies unauthorised firms known to the FCA and can include details such as websites, email addresses and phone numbers. If a victim sees a match there, they should stop contact and report the approach. If there is no match, caution is still needed. The scam may be too new to appear.

Checking permissions is just as important as checking authorisation. A firm may be authorised for one activity but not for the product being sold. For example, a firm could be authorised for insurance mediation but not investment advice. Another could be authorised in one area while a scammer uses its name to promote crypto trading, bonds, forex, contracts for difference or pension transfers. The question is not only “Is this firm on the register?” It is “Is this firm authorised to do what I am being asked to trust it with?”

Victims should also compare payment details. If the investment is supposedly with an authorised firm but the payment goes to an unrelated company, a personal account, an overseas payment processor or a crypto wallet, the mismatch matters. Scammers often explain this with words such as clearing, custody, treasury, international desk or settlement account. Sometimes those terms are real in finance. Sometimes they are fog with a bank sort code.

A sensible check should cover the firm name, FCA reference number, permissions, website, email, phone number, bank account name, product type and complaint history. This is not exciting work. Good. Excitement is overrated when someone is asking for your savings.

Reporting Routes In The UK

Scam reporting in the UK can involve several bodies because fraud cuts across regulation, policing, banking and cyber security. That can make the process feel repetitive, but each report has a different purpose.

The FCA should receive reports where the scam involves investments, trading platforms, pensions, loans, insurance, claims management, financial advice, authorised firm impersonation or an unauthorised firm pretending to provide financial services. The FCA report a scam page is the route for reporting these issues to the regulator.

Report Fraud is the main route for fraud and cyber crime reports in England, Wales and Northern Ireland. Its official site says it is the UK’s home for reporting cyber crime and fraud, and says people in Scotland should report via 101 through the Report Fraud service. Victims should use this route even if they have also reported to the FCA, because police reporting and regulatory reporting are not the same thing.

The GOV.UK guidance on suspicious emails, websites and phishing explains that people who think they have been victims of online scams or fraud can report online or call 0300 123 2040. It also gives routes for reporting suspicious emails and websites. This matters because many investment scams start with phishing, fake search ads, spoofed websites or malicious links.

The National Cyber Security Centre is relevant for phishing and suspicious messages. The NCSC phishing and scam reporting guidance explains how suspicious emails and texts can be reported. This can help get malicious sites removed and reduce harm to other people.

The victim’s bank or payment provider should be contacted separately. Reporting to the police or FCA does not automatically trigger a bank reimbursement claim. The bank needs to know what happened, when the money was sent, who received it, and why the customer believes it was a scam.

A good report should be clear, factual and detailed. It should include the timeline, amounts, payment method, recipient details, firm names, websites, emails, phone numbers, account numbers, wallet addresses, documents and screenshots. It should also state whether the scammer claimed FCA authorisation or used details from a real authorised firm.

The more organised the evidence, the easier it is for others to assess the case. This is not about writing a novel. It is about giving investigators, banks or complaint handlers enough material to act without playing detective from three blurry screenshots and a bad memory.

Compensation, Bank Refunds And Complaints

Recovering money after a scam depends on how the payment was made and who was involved. The FCA may guide victims, but the refund path often runs through banks, payment providers, the Financial Ombudsman Service or the Financial Services Compensation Scheme.

For many bank transfer scams, the key issue is authorised push payment fraud. This happens when a customer is tricked into sending money to a fraudster. The UK has moved toward stronger reimbursement rules for eligible APP scams. The Payment Systems Regulator’s APP scams reimbursement requirement introduced mandatory reimbursement protections for eligible Faster Payments APP scams from 7 October 2024, subject to rules, limits and exceptions.

That does not mean every victim will automatically be refunded. Payment type, timing, customer behaviour, warning signs, gross negligence arguments, vulnerability and claim deadlines may all matter. Still, victims should contact their bank quickly, make a formal scam claim, and ask for the decision in writing.

If the bank rejects the claim or the victim believes the bank handled the case poorly, the next step may be a complaint. The Financial Ombudsman Service fraud and scams page explains that it can consider complaints about how a bank or payment services provider acted when someone was scammed or became a victim of fraud. The Ombudsman does not chase the scammer. It looks at whether the financial business treated the customer fairly.

The Ombudsman route usually requires the consumer to complain to the financial business first. The Financial Ombudsman how to complain guidance explains that consumers should give the business a chance to sort things out before bringing the complaint to the Ombudsman. If the firm sends a final response or fails to resolve the complaint within the relevant period, the Ombudsman may then review it.

This can be important where a bank missed obvious red flags, failed to warn the customer properly, delayed action, refused reimbursement unfairly, or did not apply APP scam rules correctly. The victim should provide the timeline, evidence, bank messages, scam report numbers and why they believe the bank’s decision was wrong.

The Financial Services Compensation Scheme is a different route. The FSCS website explains that it protects customers when authorised financial services firms fail and cannot pay eligible claims. The FCA’s own claim compensation when a firm fails guidance explains that consumers may be able to claim compensation if a financial firm has gone out of business and owes them money.

The key word is eligible. FSCS does not cover every scam. If the victim sent money to an unauthorised fake broker, FSCS protection may not apply. If the victim received regulated advice from an authorised firm that later failed, FSCS may be relevant. If the loss came from a bank transfer scam, the bank and Ombudsman route may be more relevant than FSCS.

Victims should also be careful with claims management companies. FSCS is free to use directly, and paid intermediaries can reduce the compensation a person receives if a claim succeeds. Worse, scammers sometimes pretend to be recovery specialists, FSCS staff or FCA contacts. The FSCS latest scams and frauds page warns that scammers have impersonated FSCS and offered compensation in relation to investment schemes. That is the sort of thing that makes you want to unplug the internet, but it is real enough to watch for.

The practical recovery process is therefore layered. Contact the bank. Report to the FCA if financial services are involved. Report fraud through the police route. Check FSCS eligibility if an authorised firm has failed. Complain to the financial business if it may have mishandled the case. Escalate to the Ombudsman where appropriate. Keep everything in writing.

How FCA Warnings Protect Future Victims

A victim may report to the FCA and hear little about their individual case. That can feel disappointing. But reports are still useful because they help the FCA identify patterns and warn the public.

When the FCA receives information about an unauthorised firm or a clone, it can add details to the Warning List. These warnings may include names, websites, phone numbers, emails and other identifiers used by scammers. Future investors searching those details may avoid the trap.

Warnings also help banks, platforms, journalists, consumer groups and other regulators recognise scam activity. A warning does not shut every operation down overnight. Criminals can change names and domains. But a public warning creates friction. It makes the scam harder to run under the same identity.

The FCA’s wider work also pressures authorised firms to improve their controls. Banks, payment firms, e-money firms and investment businesses are expected to manage financial crime risks and treat customers fairly. FCA communications and supervision around fraud can influence how firms monitor payments, identify vulnerable customers, respond to scams and handle complaints.

For victims, this public protection role may not feel personal enough. Fair point. Nobody who has lost money wants to be told they helped produce useful intelligence. But the alternative is silence, and silence helps fraudsters. Reporting is not a guarantee of recovery, but it is one of the few ways to turn a private loss into a public warning.

How Investors Can Reduce Repeat Risk

Scam victims are often targeted again. That is one of the nastier parts of the industry. Personal details may be passed between criminals. A person who lost money to a fake broker may later be contacted by a fake lawyer, fake regulator, fake recovery firm, fake tax office or fake blockchain investigator.

The FCA will not ask for an upfront fee to release recovered money. FSCS does not charge consumers to claim directly. Police will not ask victims to move money into a safe account controlled by someone else. A recovery agent demanding more money before helping should be treated as a risk, not a lifeline.

Before dealing with any financial firm, investors should check the FCA Firm Checker, compare official contact details, search the Warning List, read permissions carefully, and avoid using links supplied by the person selling the product. The check should be done independently.

Investors should also slow down whenever an offer uses urgency. “Last chance” is not due diligence. “Guaranteed returns” is not analysis. “Private allocation” is not proof. “FCA registered” is not enough without matching details and correct permissions.

Payment details deserve special caution. Money sent to personal accounts, unrelated businesses, crypto wallets or payment apps should raise questions. A genuine investment firm should be able to explain custody, client money arrangements, fees, complaints and withdrawals clearly in writing.

Finally, investors should talk to someone before making large transfers. Scams work best when the victim is isolated. A second person does not need to be a financial expert. They only need to be outside the pressure loop. Sometimes the most useful question is the simplest one: “Why are they rushing you?”

Final Warning

The FCA helps UK scam victims by providing firm checks, warning lists, scam reporting routes, consumer guidance and regulatory oversight. It can identify unauthorised firms, expose clones and support wider action against financial crime.

It cannot guarantee refunds. Recovery may depend on banks, payment providers, FSCS eligibility, Ombudsman complaints, police reports and the evidence available.

For UK investors, the safest approach is dull but effective. Check the firm before sending money. Report quickly after suspicion. Save evidence. Use official routes. Treat recovery fee demands as fresh danger.

A scammer wants speed and confusion. The FCA system works best when victims do the opposite: slow down, verify details and report through the proper channels.